After discussing the issue on Medical (Hospitalization & Surgical) Insurance, we come to another popular type of protection - Critical Illness Coverage. Some may call it, 36 Critical Illnesses Coverage, Dread Disease Coverage, and many more.

Before we go even further, let's clear the air up so the confusion does not prolong.

When it comes to Health Insurance Protection, many are confused or even misunderstood with the differences between Medical Insurance Protection & Critical Illness Protection.

When asked, "Does your policy has Critical Illness coverage?"

The answer will be, "Yes, got cover..."

But the moment when we start reviewing their policies, we found out that there isn't any coverage on Critical Illness.

The most common confusion or mistake is that many thought that Critical Illness Protection means when they are diagnosed with any one of them, their treatment fee will be taken care of. Yes, that is right when you have Medical Insurance.

However, many has forgotten that Medical Insurance only pays the hospital (treatment fee). What about your living expenses after that? Most probably, you will lose the ability to work after diagnosed with Critical Illness. You need money to settle your Mortgage Loan, Car Loan / Hire Purchase, Daily Expenses (Food, Clothing and etc). Who is going to finance them when you lose your ability to work / ability to earn?

Critical Illness Protection

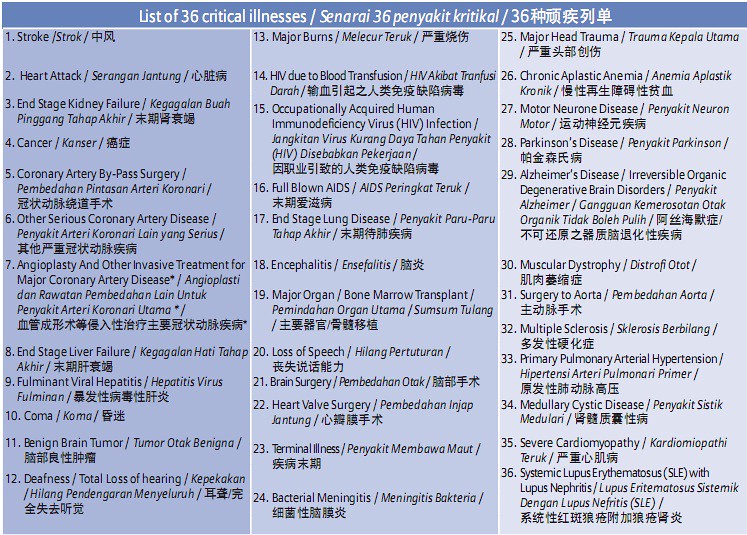

This Protection is somewhat like a Russian Roulette with 36 choices of Critical Illness. Hit any one and you will "win the reward" with the jackpot amount. Say your Critical Illness Sum Assured is RM500,000, that will be the amount you will be compensated when you are diagnosed with any one of the Critical Illness (Terms and Conditions apply). You will receive a cheque with the full amount!

If your are only insured for RM20,000, then that's too bad. Depending on the severity of your illness, it is not going to be enough. But RM20,000 is what you going to get to get through, if you ever get through at all!

Source : www.allianz.com.my (HealthCover / HealthCover Plus)

Now comes a question - How much do I need?

There is no definite answer for that question.

"You need RM1 million for your Critical Illness Protection," your Insurance Consultant will tell you.

However, my way to help you (at least) determine how much you will need is rather straight-forward.

Say you have a premonition (A strong feeling of something about to happen, esp. something unpleasant) that you are going to be diagnosed with one of the Critical Illnesses. However, when you woke up from that vision, you didn't see which illnesses you are going to be diagnosed with! Good news, at least you saw it coming before it happen, unlike your neighbour who died of stroke with no warnings and NO insurance!

So, you quickly call up your Insurance Consultant and ask her to come to your house right away. While waiting, you try very heard to search your memory to see if you can find traces of information about which illnesses you are going to get.

Your Insurance Consultant arrives and you told her about your premonition and she asked you to sign on the dotted lines. Trust me, your Insurance Consultant will look very surprised that you called to get protected!

Then you suddenly thought what if your premonition isn't true?

What if you spend all your money on Critical Illness Protection and it did not happen?

You are now stuck in a dilemma! But you finally made a decision to get as much coverage as you can afford so you will not need to change your family's lifestyle.

What if your premonition is true? Then you have to make sure your Critical Illness Protection has at least 5 times your annual income (if you are single) or 10 times your annual income (if you are married with children), simply because of the followings:

i) Daily expenses for at least 2 - 3 years in case you are not able to go back to work.

ii) Your outstanding Mortgage Loan Repayment / Car Loan or Hire Purchase Repayment

iii) Extra money to cover your spouse's income as he or she may need to opt for a job with lesser workload to take care of you. Less workload means lower income.

iv) Post Hospitalization Expenses / Traditional Chinese Medicine / Alternative Treatment - You can't be jumping up and down actively right after you discharge from the hospital. The term "critical" means no joke ya! Chances are, all these expenses may cost as much as your hospitalization bill.

Finally, after thorough consideration, you finally made a decision to get as much Critical Illness Protection as you can afford. At least an amount that will not affect your current lifestyle (if your premonition did not come true) and to have at least the protection that can help to ease you and your family (if your premonition is true).

Hope the above guideline can help you to make a better decision in determining how much you need in your Critical Illness Protection risk management portfolio.

0 comments:

Post a Comment